Omakase and luxury seem made for each other. Think about the core elements of omakase:

- An expert provides a personalised experience that is about quality, ceremony and theatre.

- The expert decides what you will have and prepares it for you. You are there from selection to the provision of the item.

- The ingredients are of fine quality (and often locally sourced).

As a trend omakase has expanded geographically with Japanese cuisine. But it has also expanded in terms of categories covered.

Koreans have taken omakase and pushed it into other areas:

- Coffee

- Dessert tasting

- Barbecue restaurants which are normally a local neighbourhood staple

- Wine and champagne-tasting

So how can omakase and luxury come together in the future?

In order to understand how omakase and luxury in the future it is worthwhile paying a good deal of attention to the pressures that the luxury industry is currently under.

Luxury is under pressure

Undoing the mistakes of the past

Luxury has expanded to be the size of industry it currently is due to ‘massification’ by most of the maisons. The exceptions to this would be the likes of Hermés.

Massification

Massification means lowering quality, using globalisation in the supply chain as well as the retail network to manufacture products cheaper. Massification occurred over a three decade period and was covered extensively by former fashion editor Dana Thomas in her book Deluxe.

Around about 2014, Gucci led the way for luxury brands to do streetwear, leading to a more accessible luxury product. Louis Vuitton did the archetypical collection with its 2017 Supreme collaboration.

Contrary to what most people believe luxury is aimed at the middle classes rather than the wealthy. But targeting middle class customers rather than the wealthy poses a number of problems:

- Increased capital outlay due to the scale required.

- Scale brings challenges in terms of supply chain management and consistency of customer experience. Greater control can be obtained by vertical integration within the supply chain and owning the retail channels. But all of this requires greater expertise and management oversight.

- Increased economic sensitivity to shocks such as interest rate and cost of living rises.

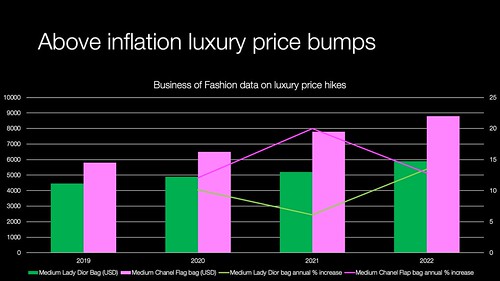

- Increased risk of devalued stock during an economic downturn. Gucci earnings were down 20 percent alone in Q1, 2024.

Bigger might not always be better over a longer view.

Secondary markets

Secondary markets have been both a boon and a bane for the luxury sector. At one time pre-owned was seen as an ‘entry-level’ product. I bought my first nice watch secondhand once it had depreciated. It was often said that the best entry-level Porsche was a secondhand one.

But gone are the days when you may buy a pre-owned Louis Vuitton purse on a second hand market stall in Paris. Now that will be on Vinted, Vestaire or some other platform.

Secondary market inflated pricing affected luxury businesses in a number of ways

- You would be interviewed to go on the waiting list for a Porsche or a Rolex.

- Authorised dealers became order takers and dealer customer service slipped.

- Your purchasing history would acquire you the rights to buy a Hermés bag over time.

Luxury groups extended their businesses into the pre-owned market. LVMH owned part of secondhand watch retailer Hodinkee. Richemont owned Watchfinder and Yoox-Net-a-Porter who sold a mix of new lines and vintage preowned items. Rolex rolled out its ‘CPO’ programme selling inspected pre-owned Rolex watches through its authorised dealer network.

Things looked really good for the luxury industry, they managed to managed to scale, to a point that LVMH is one of the largest companies in the world:

- Massification through global manufacturing supply chains.

- Keeping margins high, while letting quality go low.

- Address a rising middle class in China, Korea, Japan, the Gulf countries and Russia to counteract the hollowing out of the middle class in the US and western Europe.

- Maximising margins through controlling costs via vertical integration up and down the supply chain, from raw materials to retail.

Market change

A few things underpinned the craziness of COVID:

- Money was put in consumer pockets, for which they had few outlets.

- Supply chains were disrupted as factories closed down or pivoted to manufacturing essential products. For instances Perfums Christian Dior made hand sanitiser for hospitals for free.

A Forrester effect (also known as a bull whip effect) resulted, driving inflation that the world’s economies are coming to terms with now. Secondary effects of this event were the increased interest rates used to reduce demand driven inflation.

Other secondary effects include increased crime levels. London has gone from a luxury shoppers paradise, to having a global reputation amongst elites of being plagued by violent watch and bag robberies. COVID-19 isn’t the only driver of this crime wave, but is a contributing factor.

It has also had a catalysing effect on reducing globalisation to increase national resilience.

Consumers know that a good deal of luxury goods don’t match up with the European artisan heritage story that brands try to sell them. Experts like William Lasry has made public which brands make what kind of products where. Luxury brands often make in places like China due to capability and scale – similar reasons to why Apple products are designed in California and assembled in China. (Seriously, check out William Lasry’s channels, I love some of his visits to high-end Japanese manufacturers).

China

China has been a key focus for luxury brand, but it has changed in a number of different ways:

- Chinese consumers have changed in their confidence of native brands and have a lower opinion of many foreign brands. This is partly down to a change in attitudes called guo chao. Guo chao can be traced back to the increased confidence in the run up to the 2008 olympics in Beijing. This was partly fuelled by a series of essays published in 1996 by the likes of academic Wang Xiaodong called China Can Say Now which advocated a modern robust form of Chinese nationalism, which was in stark contrast to the Deng-era vision of globalisation and biding one’s time. In the April before the olympics Chinese consumers boycotted French supermarket brand Carrefour. Over time the negativity of these boycotts have become more-and-more performative and extra-territorial in nature. The current Xi administration has seen fit to weaponise this nationalist sentiment by directing (wrangling is a more accurate term, like cowboys with a cattle train in the Old West) public opinion to further its own ends. A more positive aspect of it has been a more open market for domestic ateliers and brands than had been seen previously. Since before 2019, there have been Chinese efforts to build a rival luxury groups to LVMH and Kering and this fits in with Xi’s distaste for irrational worship of the west.

- Xi-era growth. China under Xi Jinping faces multiple challenges around growth. The population is aging and in decline which has implications for declining consumption. Secondly economic growth has slowed compared to the double digit annual economic growth of the Deng, Jiang and Hu administrations. Foreign direct investment in China has declined for a mix of reasons including unattractive Chinese government policies, decline in China’s country brand and long term economic growth forecasts.

Regulatory change

I know what you’re thinking ok, this is very well Ged, but what does it have to do with omakase and luxury futures? Give me a little bit more time and all will be revealed.

While China is an economic superpower with a desire to export its world view and the United States is a hard and soft power super power; the European Union’s super power is legislative in nature.

European regulation drove the globalisation of the GSM mobile telephony standards during the 1990s and 2000s. They have also driven increasing internet privacy standards on web services, much to the chagrin of Alphabet, Meta and Twitter.

Now they are driving environmental standards across a range of areas including:

- A carbon tax to take into account the use of fossil fuels in extraction of raw materials, transportation, energy as an input to manufacturing and processing materials.

- Product passports from raw materials to product end-of-life encouraging a circular economy and sustainable manufacturing.

This means that the luxury sector has new restrictions on how it operates in the future.

In summary:

- We’ve likely reached peak massification due to economic and trade changes.

- Market share in China looks uncertain due to changes in consumer sentiment and tastes, meaning, a more local approach might be required or a strategic withdrawal.

- Secondary markets show that consumers are open to ownership beyond pristine new products.

- Product passports and European legislation means re-examining the whole supply chain and the data to better control it through an entire product life.

Finally, omakase and luxury futures!

Omakase and luxury look like a happy meeting in the future. Think about the tenets of omakase.

- An expert provides a personalised experience that is about quality, ceremony and theatre.

- The expert decides what you will have and prepares it for you. You are there from selection to the provision of the item.

- The ingredients are of fine quality (and often locally sourced).

Going back to go forward.

The future of luxury is about looking back. Tailors who suited generations of families and made alterations to Grandfather’s suit that the son is now wearing. The shirt maker replacing the collars and cuffs. The shoe-maker who refurbishes your shoes and has a set of lasts with your name on, for when he has to make a new set. Getting measured, having your foot cast for a last or getting your watch could be memorable events once again. So there this a precedence for expertise and service levels. But it implies a retail experience that will change dramatically.

New techniques and questions.

Previously with the exception of measuring sessions, these processes were largely concealed from the consumer and were difficult to scale. So it’s worthwhile thinking about how luxury’s omakase future could be extended with modern technology? We have some experiments that might give us some ideas. First up, L’Oreal has showcased bespoke make-up manufacture for a while.

How could high-end perfume makers adapt for products beyond make-up? Improved analysis equipment from the likes of Oxford Nanopore could facilitate individually formulated fragrance products based on skin chemistry.

Adidas experimented with its Speedfactory concept that blended the retail and shoe assembly together.

Technologically there is a lot of promising ideas. Adidas have worked with up-cycled plastics retrieved from the debris brought together by an ocean gyre made into 3d printed soles and fibres. (Look for the Parley label, who Adidas partnered with on this.)

How can additive or automated manufacturing and other processes feel luxe? In what way could they add to the theatre?

This hybridisation of retail and manufacturing changes the nature of both offline and online retail completely. Would even the largest concession in Selfridges or a shopping mall be big enough, or would fashion houses need a single purpose brand experience?

Given that there is likely to be a bit more time between manufacture and presentation of the product than there would be in a sashimi restaurant, what else would go into the maison experience? LVMH is already investing in hotels and resorts like Cheval Blanc which gives it a better understanding of more areas in luxury experience and service.

Localisation would likely to be needed to handle omakase and luxury due to culture and the need for local materials. This might include new materials, such as fungus-derived leather. Of course, this might have negative implications for luxury house supply chains, whether it’s Louis Vuitton’s iconic plastic coated leather, or the Hermés crocodile farm.

Which means that product line-ups could no longer be global in nature. So luxury companies may revisit that the creative process looks like. Should there be a single global vision anymore? Luxury maisons instincts would be to say yes, but could this be an opportunity to own local ateliers in markets like China or the US?

- Will there be more local brands instead?

- What will a maison’s heritage mean in the future? A luxury maison is about what remains the same as much as what changes. What will happen to long-standing motifs?

- Will there be a greater opportunity for more auteurs who are closer to the customers?

- How to bridge the tension in terms of choosing for the customer and creativity as well as quality?

We’re talking a very different profile of creative in terms of thinking, attitudes and skills compared to the present.

Service, repair and reuse could learn a lot lessons from traditional tailors and the service networks of watchmakers like Rolex or luggage maker Rimowa.

I could not think of a more exciting or scary time to be setting the brand direction for a luxury maison, let alone the overall direction or the likes of LVMH. But by wrapping local materials, expertise, ritual and a bit of theatre the future could look like a fusion of omakase and luxury.

More information

- Omakase adds new flavor to Seoul’s food scene | The Korean Herald

- Millennium Seoul Hilton to present tempura-only omakase – The Korea Times

- $2 convenience store lunch vs. $200 omakase: young Koreans polarised consumption | Korean Herald

- Young Koreans embrace omakase trend for desserts and beverages – Inside Retail Asia

- Deluxe – how luxury lost its lustre by Dana Thomas

- Just why are Louis Vuitton and other high-end retailers abandoning China? | South China Morning Post

- Volume and wealth make Chinese millennials a lucrative target market: GfK | Luxury Daily

- LVMH-Backed Luxury Watch Site Hodinkee Cuts a Fifth of Jobs | Business of Fashion