It makes sense to start this category with warning. Marshall McLuhan was most famous for his insight – The medium is the message: it isn’t just the content of a media which matters, but the medium itself which most meaningfully changes the ways humans operate.

But McLuhan wasn’t an advocate of it, he saw dangers beneath the surface as this quote from his participation in the 1976 Canadian Forum shows.

“The violence that all electric media inflict in their users is that they are instantly invaded and deprived of their physical bodies and are merged in a network of extensions of their own nervous systems. As if this were not sufficient violence or invasion of individual rights, the elimination of the physical bodies of the electric media users also deprives them of the means of relating the program experience of their private, individual selves, even as instant involvement suppresses private identity. The loss of individual and personal meaning via the electronic media ensures a corresponding and reciprocal violence from those so deprived of their identities; for violence, whether spiritual or physical, is a quest for identity and the meaningful. The less identity, the more violence.”

McLuhan was concerned with the mass media, in particular the effect of television on society. Yet the content is atemporal. I am sure the warning would have fitted in with rock and roll singles during the 1950s or social media platforms today.

I am concerned not only changes in platforms and consumer behaviour but the interaction of those platforms with societal structures.

Techmeme Ride Home by Techmeme on Apple Podcasts – nice summary of the biggest stories in the tech sector on a 15 minute podcast. Techmeme started as a tech focused news aggregator, but this Techmeme ride home podcast is really handy to listen to on my commute.

FK Twigs x Spike Jonze

HomePod — Welcome Home by Spike Jonze — Apple – FKA Twigs dances along in a mind bending video that’s part LSD trip and part old time Hollywood musical. Just a shame that its advertising the Apple HomePod. More related content here.

Stephen Hawking Voice Generator (play/download) ― LingoJam – kind of like the Speak n Spell you had when you were a kid but more adaptable. Hawking came to view his voice generator as part of his personality. When it was glitching out at the end of its natural life, a tremendous effort was put into replicating its sound for Hawking. The story in itself says a lot about how we relate to technology.

Let’s Go Twitter – I haven’t watched a film at the cinema in a while so am probably way late to this creative. I ended up being really confused by this advert. Visually, its a feast for the eyes, but still confusing. I love Twitter but good lord do they honestly think that advertising will solve what they seem to have diagnosed as a UX issue in on boarding for a new account?

Supermarket chain REWE empowered shoppers to choose the sugar content of its own-brand chocolate pudding. During the campaign, REWE distributed puddings that had 20%, 30%, and 40% less sugar alongside its original formula; the favorite formula (30% won!) will be permanently available for sale at the supermarket. Of course, one could say that there is a bias in the survey design, but this idea of co-creation and a transparent discussion about sugar is a welcome change. via Trendwatching.

Sometimes the most straightforward posts take the longest to write. When I started on this one last week the big question in the minds of people who watch the big advertising conglomerates is are WPP numbers a company problem or an industry problem?

WPP is looking to simplify its structure with a view to becoming a more agile and transparent business from a client perspective.

Or as it was put in the New York Times

WPP plans to accelerate a programme to simplify the business by aligning digital systems, platforms and capabilities to provide bespoke teams for its clients as opposed to the different agencies that currently compete with each other to win contracts.

Other conglomerates, notably Publicis had already started on this path when it started realigning the group under the ‘Power of One’ vision. WPP is bigger with a fuller offering and wider range of specialisms than many of its peers, no one can be under the illusion about the size of this undertaking.

Let’s talk about the tectonic plates shifting around beneath the feet of ALL the large advertising and marketing combines:

Interpublic Group (IPG)

Omnicom

Havas

Publicis

WPP

Dentsu

The tectonic plates are:

The Four

Amazon

The decline of brand marketing

The new competition

The Four

The Four is a label that Professor Scott Galloway put on Apple, Amazon, Google and Facebook. All of whom he considered to be monopolists that created value for their shareholders by putting the ‘real world economy through a shredder.

In this case I would swap out Amazon and Apple for Alibaba and Tencent, but the allusion to a quartet of horsemen portending a digital apocalypse is a useful allegory for the advertising and marketing sector. Amazon deserves a section of its own later.

Galloway’s predictions of their destructive power led to an accurate prediction of WPP’s share price tumble this week. (see the video below)

Correlation does not prove causality however — it doesn’t mean that he got the right numbers for the right reasons.

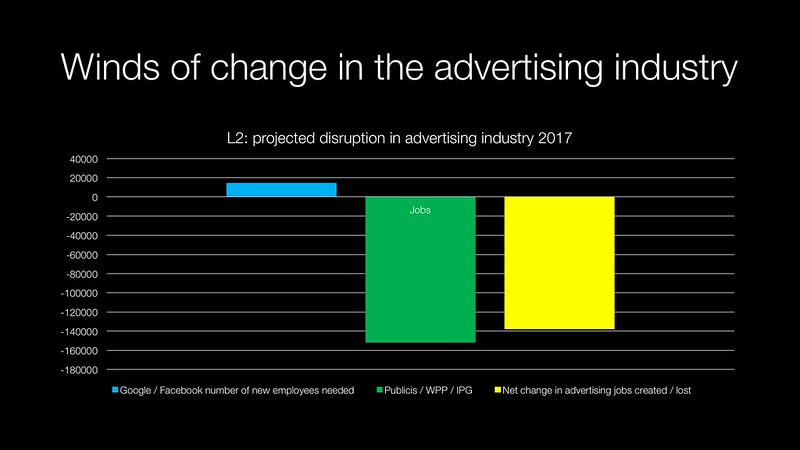

Depending whom you believe Facebook and Google are responsible for 90 percent of online advertising growth outside of China. This represents a massive concentration of media power. It has implications for the creative and planning functions of an agency. Google and Facebook also run much of the advertising technology that purchase are made on. This has decimated much of the advertising technology sector and made it harder to differentiate media planning and buying based on the technology stack.

L2 came up with this research last year based on Google and Facebook revenue targets. If they hit their numbers they would be treating around 14,193 jobs. But it would mean that the corresponding projected number of jobs lost in the advertising industry would be roughly the equivalent of every man and woman around the world employed at vehicle maker Nissan. And that’s just 2017.

L2’s calculations don’t take into account China where the advertising industry has been digitising at a much faster rate than in the west with the bulk of growth going to companies controlled by Tencent or Alibaba.

Given that most of the agencies within WPP and its peers operate on a billable hour model; this represents a considerable potential loss of value. Since the number of people directly equates to revenue.

The consolidation of online media also means that many clients will look to take back control of their media planning and buying process. The argument goes something along the lines of ‘a consolidated media landscape allows for consolidated buying by a global media trading desk due to the inherent simplicity in suppliers. The data comes from the inhouse data management platform and the media vendor (Facebook, Google, Tencent or Alibaba)‘.

The always on creative needed to fuel this process is also being increasing done in inhouse studios, in partnership with their creative agencies as a kind of hybrid model.

This is what Marc Pritchard meant when he talked about taking back control of Procter & Gamble’s marketing as part of a process to save $1.2bn by 2021. In the latest financial results, WPP claimed that their media buying margins had not suffered – only creative had.

Amazon

At the time of written Jeff Bezos is worth about 112 billion dollars, or just under double the annual defence budget of the UK for 2018. Amazon impacts the advertising and marketing industry in multiple ways.

It is starting to become a big player in online advertising in its own right. I think it would be fair to say that this competition to Google is welcome for the marketing conglomerates judging by Sir Martin Sorrell’s commentary on the likes of CNBC.

Amazon has decimated the high street. Toys R Us, Borders Group, Tower Records, Radio Shack, Maplins are just some of the names which have disappeared. It took a good number of years for people to realise that retailers are locked in a zero sum game when Amazon competes against them. Amazon has unique access to exceptionally cheap capital via its shareholders. There have been companies who have beaten it back like Alibaba’s Taobao and TMall in China. But the company has built up a huge amount of retail power and decimated brands that would have been advertising agency clients.

Amazon has become the default search engine for buying things. This has already displaced up to 20 percent of Google searches depending on whom you believe. It also means that they can place imitation goods and private label goods against branded products.

Amazon has got great data. Amazon has data at the centre of its business what consumers like, what they don’t like, what sells well on marketplace resellers. This has driven a number of the product decisions:

Increasing customer basket sizes

Expanding into new areas by screwing over marketplace resellers

Focusing their efforts on private label products which directly impacts branded products across categories. Amazon Basics is the most obvious private label to consumers, but there are many more where the link isn’t so obvious

Depending on your brand category the answer may be:

Owning your own retail chain like Apple or LVMH’s DFS Group

Direct sales and subscription services have piqued the interest of FMCG brands like Dollar Shave Club

All of this impacts the advertising sector. For more information on the power of Amazon, I can recommend Scott Galloway’s The Four.

The decline of brand marketing

The relative decline of brand marketing has been driven by a number of factors, some of these factors are good and some aren’t.

Let’s talk about the good reasons first of all.

‘Performance marketing’ driving customers directly to a sale has been transformed by the rise of modern online advertising techniques including search advertising and retargeting. Retailers can zero in on intent to a much greater degree than shopping television or direct response print adverts ever could. Google and social media have turned into reputation platforms which then displayed below-the-line spend from the likes of public relations agencies. This was happening at a time when journalist employed by publications have declined; implying a natural progression

At least some consumers can’t be reached through traditional media channels with sufficient frequency for brand advertising. Social media, online video and banner ads make sense as part of an omnichannel approach

The bad reasons:

The focus on ROI rather than profits has meant that a balance longer term brand building and shorter term sales has fallen out of kilter. Marketing then becomes a reductive process. To use a farming analogy; its like moving from arable farming with crop rotation to slash and burn. This is particularly noticeable in the way private equity management has affected fast moving consumer brands under its control. Zero-based budgeting is seen as a source of cost cutting rather than ensuring the efficient and effective use of marketing resources

Digital first strategies – for many marketers this has meant a move from media-neutral, let the communications problem define the channels used to a digital dogma. I make my living with digital media, but I recognise the flexibility required in thinking to deliver an effective strategy

It isn’t about one approach over another but finding balance that works for sales now and in the future.

The new competition

The rise of digital advertising has seen business services expand ways that we couldn’t predict. Advertising agencies like Ogilvy understood the potential for digital early on. Consultancies were focused on systems integration and the use of technologies to change business functions. As they became interconnected internally and externally; the progression into marketing made sense.

A reduction in creative budgets caused marketing agencies to move into areas like service design. Consultancies have looked to inject creativity into their values and skills set by mirroring the kind of acquisition strategy that built the marketing conglomerates.

In the meantime technology companies, notably Adobe have treated marketing like any other business function with a sale conducted at the c-suite level just like Oracle or similar. In many respects this move is understandable as companies use a data management platform (DMP) to derive audience insights and improve their digital marketing. This isn’t vastly different from historic data warehousing and data mining applications.

The enterprise software companies allow large companies to do internally what they have previously asked media agencies to do.

WSJ City | Five signals sent by China’s Anbang takeover – Reining in big spenders (spending capital abroad in an untargeted manner), reduction of systemic financial risk, concern over complex short-term high-yielding wealth products

Opinion | The Tyranny of Convenience – The New York Times – Americans say they prize competition, a proliferation of choices, the little guy. Yet our taste for convenience begets more convenience, through a combination of the economics of scale and the power of habit. The easier it is to use Amazon, the more powerful Amazon becomes — and thus the easier it becomes to use Amazon. Convenience and monopoly seem to be natural bedfellows. – great article by Tim Wu

Burson Cohn & Wolfe – SixtySecondView – like any other business merger the focus will keep the eye off the ball at a time when the PR industry is seeing exceptionally low growth rates. I have friends and former colleagues on both sides of this in both Asia and Europe; so I hope it works out well.

Smart homes and vegetable peelers — Benedict Evans – interesting starting point, but I think that there should be a second layer. Can the intelligence be local (like lighting sensors based on movement and presence in office buildings) or does it need cloud computing? Why can’t smart lightbulbs be at the edge rather than in the cloud. Why does a Nest thermostat need to be in the cloud?

Samsung says it’s going to stop pumping out features and start making devices good instead – BGR – “We developed mobile phones earlier than China, and we were obsessed with being the world’s first and industry’s first rather than thinking about how this innovation would be meaningful to consumers,” Koh said. “Being the first turns out to be meaningless today, and our strategy is to launch something that consumers believe meaningful and valuable at a right time.” – this reads like a slap in the face to Huawei’s approach on innovation and features

Wow. Facebook eroding much faster than anyone expected. Pivotal’s analysis of Nielsen data shows core app dropped 11% in time spent per person in November. Without Instagram/WhatsApp, a complete cliff dive in share of time. pic.twitter.com/tEd5UclZ3p

The tweet about Facebook eroding is part of a greater issue of what Facebook is calling internally ‘context collapse‘. Facebook recognised the issue back in 2015. There are several likely reasons for Facebook eroding:

Negative network effects

Societal norming on social media content

Lack of trust in the facebook brand

People just don’t like Facebook as a platform that much

Nokia on 5G at MWC, what struck me is the sales pitch was more like an enterprise software company like IBM or Oracle than a telecoms vendor. There is lots of tech in the networks but there isn’t a recognisable killer app. His warnings about 5G upgradeable products ring true though.

Consumer behaviour

Asian Boss do some really nice street interviews in different Asian cities and this one about Apple iPhones in Korea is particularly instructive. Samsung is seen as the default phone as they assemble phones (mostly for Asian markets) in Korea. Whereas in Europe all of the are made in China. When I lived in Hong Kong, both Samsung and LG emphasised that they made their phones in Korea with an implicit quality guarantee.

The iPhone seems to have won out on product design amongst younger people. but one shouldn’t ignore the desire to support the national brand.

I was having an online conversation with friends in the game about our favourite advertising, and this one came up. I hadn’t seen it before. It’s a public service announcement from New Zealand: Blazed – Drug Driving in Aotearoa.

Guinness Rutger Hauer ads

I also managed to find all the Rutger Hauer ‘Pure Genius’ ads done for Guinness. A lot of it looks like fresh thinking but mainstream production now due to CGI and After Effects, but at the time it was like nothing else that you would have seen

Nazira

I have been listening to this mix by Nazira. Nazira is from Almaty, Kazakhstan and plays at Berlin’s Room 4 Resistance parties. There’s also a great interview with her on the Discwoman site

Revisiting For A Few Dollars More – I love the pace, the way it was shot and the storytelling. It also has Lee Van Cleef and Clint Eastwood teaming up – EPIC. When I was a child I was confused the Lee Van Cleef playing two different characters in the ‘Dollars Trilogy’. In The Good, The Bad and The Ugly he plays a psychopathic gun for hire. In For A Few Dollars More he plays the honourable Colonel Mortimer looking for justice against a bandit.

Gian Maria Volontè played both protagonists in A Fistful Of Dollars and For A Few Dollars More – and died both times. Leone didn’t intend for the films to be a trilogy, but they work quite well together. More related content here.