Two big consumer orientated companies: Weight Watchers and Kraft Heinz announced financial losses.

Why is this significant?

Consumer good marketing is in more turmoil than it has been for a long time. Millennial-led memes are changing the environment for consumer goods brands:

- Authenticity

- Natural trumps anything else for health

- Body positivism

There are also some structural and competitive issues:

- Private label brand expansion; in particular Amazon

- Online retailing disrupting traditional shopper marketing

- Amazon’s advertising offering

- Horizontalism

- Subscription and delivery services

- New product models

Authenticity

Authenticity is something that has become at the centre of culture. In a time when social channels and media have painted an artificial life and traditional marks of success are hard to attain ( like home ownership) experiences became important. It wasn’t enough for products to fill a need; they also need to have a story with heritage behind them. Brands have become started by ‘real people’ who’ve become influencers in areas such as make-up.

The good news is that authenticity isn’t anti-brand, in fact the notion of credibility that you would have heard 20 years ago no longer has resonance. Naomi Klein’s No Logo or becoming a ‘sell out’ celebrity no longer resonate.

The challenge of authenticity changes by category:

- Processed food: considered not authentic by their synthetic nature, food delivery services and DIY meal packs act as alternatives

- The move to beards has adversely affected shaving products, hence the Gillette pivot to women and Unilever’s bizarre adverts to encourage male body hair shaving

- Beauty products: Authenticity has supported the launch of niche brands by influencers. This is rather different to the likes of previous brands like Gloria Vanderbilt | Murjani Corporation tie up to launch the first designer jean brand in the late 1970s

Natural trumps anything else

In the 1980s and 1990s we saw a take off in healthier foods from artificial sweeteners to margarines that have more beneficial properties in preventing heart disease. Butter and cheese were seen as unhealthy products. Jump forward to today. Sugar whilst not considered good, is considered a better product than artificial sweeteners. High fructose corn syrup is considered to be the great satan of sweetness.

Now butter is back in. Margarine is losing market share year-on-year, which is the reason why Unilever divested its margarine business. Consumers looking for vegan options look towards nut butters and coconut oil. Polyunsaturate fats just don’t matter that much any more.

TV dinners are losing out to recipe packs; where a set of fresh ingredients and a recipe are supplied to consumers instead of microwave heated processed meals. From Kraft Mac and Cheese to Uber Eats delivered macaroni and cheese.

All of the brands, manufacturing process and supply chain prowess are problematic for consumer goods giants.

Body positivism

Consumers continue to flock to a fitness movement, that would be familiar to consumers in the 1980s. Health and fitness has become ever more professional with a fetishisation of high protein diets.

In parallel to this has come along a move towards being more accepting of people regardless of their shape. This body positivism moves the dialogue away from weight loss and fitness as a health requirement to a broader lifestyle and mental wellness positioning.

More realistic body shape models is reducing the social pressure on weight control and dieting. Working out is more about performance and strength in terms of emphasis. Again all of this impacts food formulations further.

Body positivism means that a proportion of the population have ‘permission’ to indulge: which probably explains the popularity of comfort food like American diner fare and dessert restaurants.

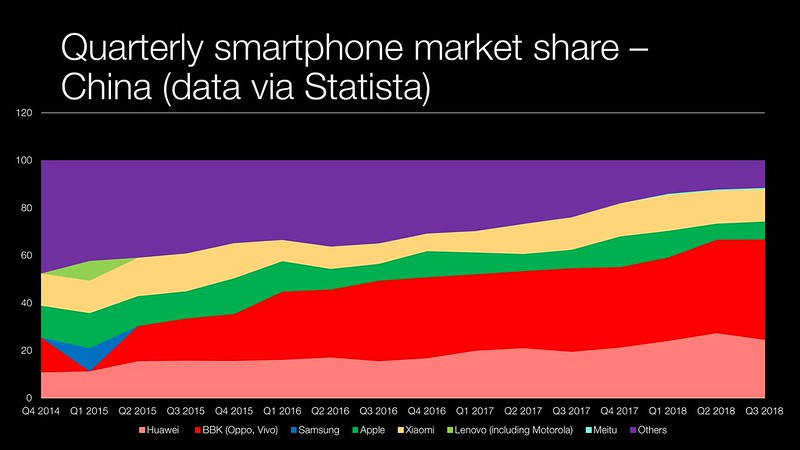

Private label expansion

Discount stores like Aldi have gone from 2% of UK retail sales to over 7.5% last year. They focus on private label brands and only a third of the SKUs presents challenge to traditional grocery retailing. And brands already have had an uneasy relationship with mainstream supermarket private label brands that culminated in legal action like the Penguin | Puffin legal case back in 1997.

One of the most amazing things about Amazon is how it has utilised its retailing data to target and launch a plethora of private label brands across sectors at a phenomenal pace.

Horizontalism

Over a decade ago now, I worked at a creative agency and we were asked to pitch by a new premium crisp (American English: potato chip) brand. They were similar to the Kettle Chip brand. The key difference was that they didn’t own the production facility. Their manufacturing partner was a private label manufacturer for supermarkets, but didn’t compete in the branded product space.

The brand had worked with their manufacturing partner on new product development and were bringing their own marketing and branding expertise. All the big consumer companies have seen marketers get their knowledge and knowhow with them before moving off and forming these upstart brands. The brand managed to piggy back on someone else’s logistics channels.

By comparison the likes of Mondelez have their own factories and logistics to reach their retail partners. Infrastructure provides quality and cost controls at scale but put restrictions on new category entry and new product development.

That means that putting a product into the market takes time and costs more money to happen. Move forward ten years with Amazon and direct online sales becoming easier, you are seeing upstart brands taking advantage of horizontal services.

It is similar to the business model that Nike rolled out in sportswear during the 1970s and how the computer industry changed as it moved into the PC age.

Online retail disruption

Originally it was only retailers that have had to deal with the move of consumer shopping online. Supermarkets have managed to turn their retail and warehousing presence into effective e-commerce delivery with varying degrees of success. Those that didn’t do well at it like M&S and Kroger have partnered with the likes of Ocado for the technological knowhow.

Amazon has posed a threat to these retailers as the company has moved from not only being a rival retailer but a product search engine. Even stealing search volume from Google. Amazon has also rolled out private label products and proved itself to be a capable platform for new brands looking to launch consumer goods competing with the big brands.

Add into this Amazon’s advertising business and the company seems to have greater king making marketing power than the traditional large supermarket chains.

Uberisation of services has seen food delivery become a substitute product for home cooking changing consumer behaviour in a way that doesn’t favour consumer brands.

Subscription and delivery services

The speculation around the Amazon Dash launch hinted at the potential impact that subscription services could present to consumer companies. The classic model of Dollar Shave Club or Birchbox took the Book Club or Columbia House record subscription model. They moved it from direct mail campaigns and newspaper magazine direct response ads, to online and applied it to two very different consumer use cases:

- Experimentation for highly engaged consumers in areas like beauty

- Convenience for low passion products like razors

These businesses have scared the pants off consumer businesses. Gillette has experimented with its own brand subscription service for razors. Unilever went out and bought Dollar Shave Club for a $ 1 billion valuation. They also failed to buy the Honest Company which sells baby products and household goods.

The fear and sense of being displaced and disrupted by these new services is greater than their financial impact. It likely fulfils the nightmares that McKinsey and Deloitte presentations to the C-suite about digitalisation of business and disruption create.

Weight Watchers & Kraft Heinz: making their tasks more difficult

Kraft Heinz’ CMO had to deny that the company had under-invested in its brands. That statement felt eerily like the cliched moment when a football club chairman says on the record that the manager has their full support. Eduardo Luz has a tricky problem on his hands:

- He admits that what the analysts have said is true and Kraft Heinz has underinvested in brands. That’s a CMO death sentence right there, spectacular fuck-up and unlikely to get work at another significant consumer goods company

- Says that its a misconception that cost-cutting adversely affected brand investment. He is then relying on owner 3G Capital’s cuts to resurrect the business in the future. A 27% drop in market value is a big hole to fill for shareholders. Their approach is considered to have worked at Anheuser-Busch InBev and Burger King in terms of raising profits. 3G Capital are quite open about the fact that they use zero-based budgeting (ZBB)

IF they are doing ZBB properly, this is what the annual plan process should look like:

- Last year’s spend isn’t rolled over from a planning perspective – that’s the zero, essentially a blank sheet of paper. The idea is that there are no sacred cows

- There is a research aspect to the planning

- The plan is crafted promising a specific ROI and asking for a certain amount of investment

- Senior management vet the plan and come back with two possible outcomes: plan approved, or pushback and ask for changes

The benefits of ZBB

- Efficient resource allocation by focusing on needs, requirements and benefits

- Focus on operational efficiency

- Can increase collaboration and co-ordination within the firm

ZBB has its challenges

- The benefits of brand advertising deliver ROI far longer than a year, so it doesn’t measure their full impact and isn’t optimised for brand building

- Justifying every line item can be problematic for functions with intangible outputs like brand rather than direct response marketing

- In a large company, there is likely to be an overwhelming volume of information to support the budgeting process

- Time consuming

That hasn’t stopped the likes of Unilever and Proctor & Gamble adopting it.

If Luz thinks that ‘under investment’ in brands is a misconception. It seems reasonable to assume at least some of the following happened:

- The research process didn’t take account of market changes and was probably focused at a brand level on operational efficiency rather than horizon scanning

- The specific ROI promised was a misconception

- There was inadequate training put in place to effectively plan and assess with ZBB

- 3G Capital’s wrong-headed implementation of ZBB caused Kraft Heinz to focus on maximising the profitability of low growth areas through cuts and not focusing on investing sufficiently in (newer) high growth areas. These high growth areas are likely to be due to the kind of changing market dynamics outlined earlier in this post

Kraft has struggled with low growth for over a decade which was the primary business reason for buying Cadbury – a higher growth business at the time that could also be used to take Kraft into new geographic markets. 3G Capital took on a serious challenge when they merged Kraft and Heinz.

By comparison Weight Watchers seems to have had their eye on the horizon; they realised that body positivism had moved the goal posts on size and decided to refocus on health. But they thought that a rebrand rather than innovation was the way forwards. Weight Watchers weren’t fooling anyone except themselves with the move to WW and ended up with a declining subscriber base.

But there are opportunities out there for them. Imagine if there was a Weight Watchers restaurant on Deliveroo providing healthy meals cooked just for you – as an extension of their supermarket product range? Or dietary advice and for those that want to bulk up and be everything that they can be that’s more cost effective than a dietician and more trustworthy than surfing cross fit forums?

Instead they went from a brand that stood for something in the eyes of consumers, to something that was literally meaningless.