What is ESG?

ESG can be considered to be a form of ethical investing. Ethical investing of one form or another has been around for a while. In the US by the middle of the last century union pension funds were looking to invest in areas like affordable housing. There used to be funds and banks that wouldn’t invest in certain industries, such as tobacco or arms manufacturers. The Cooperative Bank in the UK screens business banking clients looking at issues such as animal welfare and supplying arms to oppressive regimes.

ESG or environmental & social governance can be seen as a way of standardising ethical investing and has been adopted by the US financial services sector. Environmental factors have been raised in importance due to concern about climate change. ESG as we now know it came out of the UN Principles for Responsible Investment which financial institutions signed up to. This happened in 2005 and by 2016 it became a ‘hygiene factor for asset managers as requests for proposals required being a UN PRI signatory.

The PRI is based around six principles

- Incorporation of ESG issues into investment analysis and decision-making processes – this makes sense to a point. What are the best decisions from an environmental and social governance point of view is a matter of perspective as every decision requires trade-offs. The same kind of ‘religious’ disputes that caused Greenpeace to be formed by ex-Sierra Club members now drive ESG decisions. Here’s a hypothetical example. Internal combustion engine cars have a lower carbon footprint of manufacture than their electric counterparts. 70 percent of a vehicles carbon footprint is in its manufacture. Therefore I could argue investing in a secondhand vehicle supermarket a la AutoTrader or BringATrailer would be better than Tesla Motors. The reality is that Tesla tells a great story and the optics my valid rational argument for an investment decision would go down badly with the media and many investors.

- Being active owners and incorporate ESG issues into our ownership policies and practices. So should investors be looking to get companies to divest oil production? Or should they be running down their oil fields in a responsible manner? If they divest their oil production, it could be going to custodian that would have less moral and social scruples. Again the optics on these decisions may drive a move that on balance would be worse for the environment.

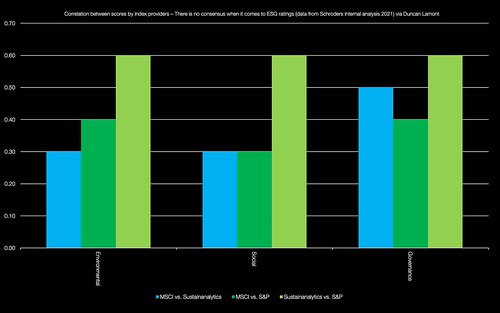

- Seeking appropriate disclosure on ESG issues by the entities in which we invest.

- Promoting acceptance and implementation of the Principles to their peers within the investment industry. Which is why Larry Fink is doing these kind of interviews on business media.

- Work together to enhance effectiveness in implementing the Principles.

- Reporting on activities and progress towards implementing the Principles. If you dig into back and investment fund websites you will be able to find these reports for listed companies, financial institutions and even the likes of Harvard University

Why do investors use ESG?

ESG investing is considered to be a form of risk management

The rationale being that ESG aligns with companies there that are prepared for risks that other companies miss. However it is based on a fallacy that other people are stupid, rather than the risks not matching their client’s investment horizons.

Companies that have embraced sustainability are doing better

This is based on a perception that ‘virtuous investments’ as a strategy tend perform better than sinful ones. Yes there are a number of businesses in this category. Sinful companies can do well as well, and ESG investment funds don’t necessarily outperform their rivals.

An altruistic desire to drive down the cost of capital for green businesses versus their incumbent competitors in the carbon economy

Going down this route requires an admission that this might not outperform as an investment and won’t be a substitute for political, legal and regulatory action to spur economic greening.

ESG Earthquake

On August 2, 2021, Tariq Fancy dropped a proverbial bomb on the ESG sector. He didn’t say anything that hadn’t been said before. But the way he put it together into a cohesive story and the authority he had to talk about ESG made an impact.

Fancy comes from a background in investment banking, private equity and fund management. Most notably he formerly worked for BlackRock as their global chief investment officer for sustainable investing. In other words, he knew the ESG investment business inside-and-out.

What I considered to be his most relevant points were:

- The tension between ESG lowers the cost of capital to green businesses, lowering investor returns. But are promoted as good performers by funds

- ESG investments have long term time horizons that don’t match the requirements of investors. This creates a misalignment between profit and purpose. A secondary aspect of ESG investment being weak means that there will never be a critical mass of capital to make it work

- People thinking that their retirement plan is going to help the world; stops them taking actions in their own lives that might help changing the world. (It’s the investment equivalent of liking or sharing the Kony 2012 video and expecting real political change in Sierra Leone)

- Can you trust people on Wall Street or in the Square Mile to decide what is good for society?

More ethics related content here.

More information

Roberts, B.C., Trade Union Government and Administration in Great Britain (Harvard University Press, 1958)

Investment Division, Directorate for Financial and Enterprise Affairs, The UN Principles For Responsible Investment And The OECD Guidelines For Multinational Enterprises: ComplementarIties And Distinctive Contributions (OECD, 2007)

Porter, M.E., Serafeim, G., Kramer, M., Where ESG Fails (International Investor, October 16, 2019)

Fancy, T., The Secret Diary of a ‘Sustainable Investor‘ (Self published, August 2021)